Mortgage Rates Jump to Highest Level in Nearly a Month as Inflation Fears Shake Housing Market

Mortgage rates are climbing again — and the housing market is feeling the pressure.

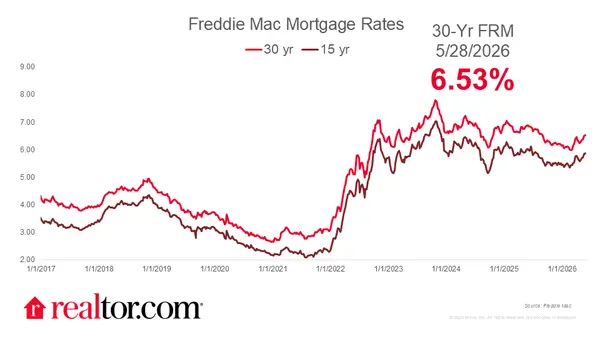

Recent economic uncertainty and renewed inflation concerns tied to global conflict have pushed mortgage rates to their highest level in nearly a month, creating another hurdle for homebuyers already navigating affordability challenges.

While buyers had started adjusting to rates in the low-to-mid 6% range earlier this year, the latest increase is once again testing affordability and buyer confidence heading into the summer housing season.

Why Mortgage Rates Are Rising Again

Mortgage rates are heavily influenced by inflation expectations and the bond market.

Recently, fears surrounding global instability and ongoing war-related economic disruptions have increased concerns that inflation could remain elevated longer than expected. When inflation fears rise, bond yields typically climb — and mortgage rates tend to follow.

As a result, the average 30-year fixed mortgage rate has moved noticeably higher over the past several weeks.

Even relatively small rate increases can have a major impact on affordability.

For example:

- A 0.5% increase in rate can raise monthly payments significantly

- Buyers may qualify for less home

- Debt-to-income ratios become tighter

- Cash-to-close requirements can increase

For many households, affordability is becoming just as important as home price itself.

Buyers Are Adapting — But More Cautiously

Despite rising rates, buyers have not disappeared from the market entirely.

Instead, many are becoming more strategic and payment-focused.

Today’s buyers are:

- Negotiating harder

- Comparing financing options carefully

- Exploring rate buydowns

- Looking at smaller homes or different locations

- Taking longer before making offers

The emotional urgency that drove the housing market during previous years has slowed considerably. Buyers are no longer waiving every contingency or rushing into homes within hours.

Instead, many are prioritizing financial stability and long-term affordability.

Higher Rates Are Reshaping Seller Expectations

Sellers are also starting to feel the impact of elevated mortgage rates.

Homes that would have received multiple offers instantly a few years ago may now sit longer unless priced correctly. Buyers are more selective, and overpriced homes are facing increased competition from newer listings and builder inventory.

This shift is creating a more balanced market in many areas.

That balance can benefit buyers through:

- Seller-paid closing costs

- Interest rate buydowns

- Price reductions

- Repair negotiations

- Increased inventory choices

While affordability remains difficult, buyers often have more negotiating power today than they did during the ultra-competitive market of 2021 and 2022.

New Construction Builders Continue Offering Incentives

Builders are responding aggressively to higher rates in order to keep sales moving.

Many new construction communities are offering:

- Temporary rate buydowns

- Closing cost incentives

- Flex cash

- Appliance packages

- Lower lot premiums

- Special financing programs

In some situations, buyers are finding lower monthly payments through builder incentives than they would purchasing comparable resale homes.

This is one reason new construction has remained relatively resilient even as mortgage rates fluctuate.

The Housing Market Is Becoming More Stable — Not Crashing

Higher mortgage rates are certainly slowing parts of the market, but current conditions are very different from the 2008 housing crisis.

Today’s market still has:

- Limited long-term housing inventory

- Strong homeowner equity

- Stricter lending standards

- Stable employment overall

- Ongoing buyer demand

Rather than collapsing, the market appears to be transitioning into a slower, more normalized environment where pricing, negotiation, and affordability matter more again.

For buyers, that means patience and strategy are becoming far more valuable than speed.

What Buyers Should Focus on Right Now

Trying to perfectly time mortgage rates is extremely difficult.

Instead of waiting endlessly for rates to drop dramatically, many successful buyers are focusing on:

- Purchasing within a comfortable monthly payment

- Negotiating seller concessions

- Using temporary buydowns

- Choosing homes that fit long-term goals

- Refinancing later if rates improve

The reality is that when rates eventually decline, competition could increase rapidly again — potentially driving prices higher and reducing negotiating leverage.

Final Thoughts

Mortgage rates are climbing again — and the housing market is feeling the pressure.

Recent economic uncertainty and renewed inflation concerns tied to global conflict have pushed mortgage rates to their highest level in nearly a month, creating another hurdle for homebuyers already navigating affordability challenges.

While buyers had started adjusting to rates in the low-to-mid 6% range earlier this year, the latest increase is once again testing affordability and buyer confidence heading into the summer housing season.

Why Mortgage Rates Are Rising Again

Mortgage rates are heavily influenced by inflation expectations and the bond market.

Recently, fears surrounding global instability and ongoing war-related economic disruptions have increased concerns that inflation could remain elevated longer than expected. When inflation fears rise, bond yields typically climb — and mortgage rates tend to follow.

As a result, the average 30-year fixed mortgage rate has moved noticeably higher over the past several weeks.

Even relatively small rate increases can have a major impact on affordability.

For example:

- A 0.5% increase in rate can raise monthly payments significantly

- Buyers may qualify for less home

- Debt-to-income ratios become tighter

- Cash-to-close requirements can increase

For many households, affordability is becoming just as important as home price itself.

Buyers Are Adapting — But More Cautiously

Despite rising rates, buyers have not disappeared from the market entirely.

Instead, many are becoming more strategic and payment-focused.

Today’s buyers are:

- Negotiating harder

- Comparing financing options carefully

- Exploring rate buydowns

- Looking at smaller homes or different locations

- Taking longer before making offers

The emotional urgency that drove the housing market during previous years has slowed considerably. Buyers are no longer waiving every contingency or rushing into homes within hours.

Instead, many are prioritizing financial stability and long-term affordability.

Higher Rates Are Reshaping Seller Expectations

Sellers are also starting to feel the impact of elevated mortgage rates.

Homes that would have received multiple offers instantly a few years ago may now sit longer unless priced correctly. Buyers are more selective, and overpriced homes are facing increased competition from newer listings and builder inventory.

This shift is creating a more balanced market in many areas.

That balance can benefit buyers through:

- Seller-paid closing costs

- Interest rate buydowns

- Price reductions

- Repair negotiations

- Increased inventory choices

While affordability remains difficult, buyers often have more negotiating power today than they did during the ultra-competitive market of 2021 and 2022.

New Construction Builders Continue Offering Incentives

Builders are responding aggressively to higher rates in order to keep sales moving.

Many new construction communities are offering:

- Temporary rate buydowns

- Closing cost incentives

- Flex cash

- Appliance packages

- Lower lot premiums

- Special financing programs

In some situations, buyers are finding lower monthly payments through builder incentives than they would purchasing comparable resale homes.

This is one reason new construction has remained relatively resilient even as mortgage rates fluctuate.

The Housing Market Is Becoming More Stable — Not Crashing

Higher mortgage rates are certainly slowing parts of the market, but current conditions are very different from the 2008 housing crisis.

Today’s market still has:

- Limited long-term housing inventory

- Strong homeowner equity

- Stricter lending standards

- Stable employment overall

- Ongoing buyer demand

Rather than collapsing, the market appears to be transitioning into a slower, more normalized environment where pricing, negotiation, and affordability matter more again.

For buyers, that means patience and strategy are becoming far more valuable than speed.

What Buyers Should Focus on Right Now

Trying to perfectly time mortgage rates is extremely difficult.

Instead of waiting endlessly for rates to drop dramatically, many successful buyers are focusing on:

- Purchasing within a comfortable monthly payment

- Negotiating seller concessions

- Using temporary buydowns

- Choosing homes that fit long-term goals

- Refinancing later if rates improve

The reality is that when rates eventually decline, competition could increase rapidly again — potentially driving prices higher and reducing negotiating leverage.

Final Thoughts

Mortgage rates reaching their highest point in nearly a month is another reminder that today’s housing market remains highly sensitive to inflation and global economic uncertainty.

But even with higher rates, buyers are still active — just far more cautious and strategic than before.

Today’s market rewards preparation, smart financing, negotiation, and long-term planning. Buyers who stay informed and flexible may still find strong opportunities, especially as sellers and builders continue adjusting to changing market conditions.

Mortgage rates reaching their highest point in nearly a month is another reminder that today’s housing market remains highly sensitive to inflation and global economic uncertainty.

But even with higher rates, buyers are still active — just far more cautious and strategic than before.

Today’s market rewards preparation, smart financing, negotiation, and long-term planning. Buyers who stay informed and flexible may still find strong opportunities, especially as sellers and builders continue adjusting to changing market conditions.

Categories

Recent Posts