Buying a Home in 2025 Is Expensive — But So Is Renting. Which Costs More Long-Term?

💰 Rent vs. Buy in 2025: Which Really Costs More?

If you’re stuck between renting and buying this year, you're not alone. With mortgage rates still hovering near 6.7% and rents holding steady or rising in many cities, the math isn’t easy. But the decision isn't just about monthly payments—it's about your lifestyle, goals, and long-term value.

Let’s break it all down so you can make the smartest move in 2025.

🏘 The Big 2025 Housing Reality: It’s Not Cheap Either Way

According to a recent study by Realtor.com, in 48 of the 50 largest U.S. metros, renting is cheaper than buying—by an average of 38% monthly. In some high-cost cities like San Francisco or Seattle, the difference can be even larger.

Yet even though renting may feel easier short-term, buying still offers long-term financial upside—especially if you stay put for at least 5 years and plan to build equity.

📊 Real Cost Comparison Example (Monthly)

Let’s take an average mid-tier metro like Orlando, FL in 2025:

| Scenario | Renting | Buying (10% down, 6.7% rate) |

|---|---|---|

| Monthly Payment | $1,900 (2 bed apt) | $2,750 (incl. taxes/insurance) |

| Upfront Costs | ~$3,800 (2 mo. rent + deposit) | ~$35,000+ (down payment & closing) |

| Maintenance | Included in rent | ~$150/mo avg |

| Equity Built | ❌ None | ✅ ~$7,000+ after year 1 |

Source: Zillow, Rent.com, Freddie Mac averages

✅ When Renting Makes Sense

-

Short-term living plans (less than 3–4 years)

-

Lower cash on hand for down payments or reserves

-

Remote workers who may relocate again soon

-

You want no home maintenance responsibility

-

You prefer more flexibility

🏡 When Buying Makes Sense

-

You’re planning to stay in place for 5+ years

-

You want to build wealth through home equity

-

You’re financially ready for down payment & maintenance

-

You’re tired of annual rent increases

-

You’re buying in a fast-growing area with future value upside

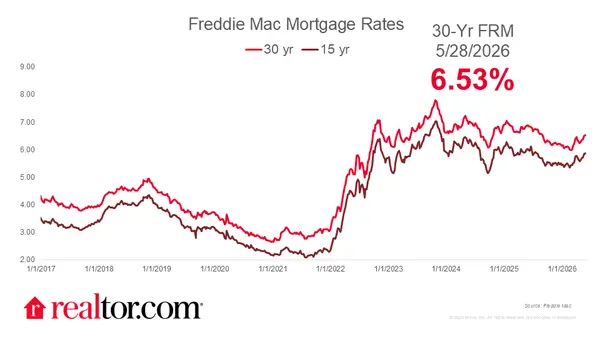

📈 Mortgage Rates in 2025: A Major Factor

While mortgage rates peaked near 7.5% in 2023, they’ve hovered around 6.6%–6.9% throughout 2025 so far. That means monthly mortgage payments are significantly higher than just two years ago.

Still, many experts forecast rates may decline slowly into 2026—making it possible to refinance later after locking in your home today.

🧠 Long-Term View: Equity > Monthly Cost?

Even though renting can save money monthly, it doesn’t build wealth. Owning gives you:

-

Forced savings via equity

-

Home appreciation potential

-

Tax write-offs on mortgage interest (if eligible)

-

A stable housing cost once your rate is fixed

📊 2025 National Snapshot

| Factor | Renting (avg) | Buying (avg) |

|---|---|---|

| Monthly Housing Cost | $1,750 | $2,500–$2,900 |

| Equity Gain (Year 1–3) | $0 | $15,000–$25,000 |

| Flexibility | High | Low |

| Upfront Cost | Low (~$3k) | High (~$25k–$50k) |

| Maintenance Responsibility | None | You |

| Stability | Low (rents increase) | High (fixed mortgage) |

🤔 Still On the Fence?

If you're still unsure, ask yourself:

-

Can I comfortably afford the monthly cost and emergency repairs?

-

Am I staying in this location for at least 5 years?

-

Am I okay waiting to build equity, or do I need flexibility now?

There’s no right or wrong answer—just the right answer for YOU.

📍 Final Thoughts

In 2025, both renting and buying come with pros and cons. Renting may be cheaper monthly, but buying can help you build wealth and lock in your housing future. If you’re stable, ready, and planning long-term, buying may still be the best investment. But if flexibility and affordability are your priorities right now, renting might buy you the time and space you need.

Categories

Recent Posts